Understanding the Different Types of Mortgages: Choosing the Right One for Your Home-Buying Journey

Higher Education

Higher Education

Welcome to the third installment of our Monday Mortgage Matters series! Today, we’re tackling a key topic that can feel overwhelming for many homebuyers: the various types of mortgages. With so many options available, it's easy to get confused about which loan best suits your needs. But don’t worry—by the end of this post, you'll have a clear understanding of the most common mortgage types and the information you need to make an informed decision that fits your unique situation.

Your first choice when selecting a mortgage will typically be between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). Let’s break down the key differences, pros, and cons of each.

A fixed-rate mortgage offers consistent interest rates for the entire loan term, whether that’s 15, 20, or 30 years. This means your monthly payments will remain the same, making budgeting more predictable.

Pros:

Cons:

Who Should Consider a Fixed-Rate Mortgage?

If you plan on staying in your home long-term and want stable, predictable payments, a fixed-rate mortgage is ideal.

An ARM offers a lower initial interest rate for a set period—usually 5 or 7 years—before the rate begins adjusting periodically based on market conditions.

Pros:

Cons:

Who Should Consider an ARM?

If you plan to move or refinance within a few years, an ARM could be a great option for lower initial payments.

Once you’ve decided on a fixed or adjustable rate, you’ll need to choose between a conventional loan or a government-backed loan, like FHA, VA, or USDA loans. Each has its benefits depending on your situation.

Conventional loans are not insured or guaranteed by the federal government. They typically require higher credit scores and larger down payments, but they offer more flexibility and potentially lower costs in the long term.

Pros:

Cons:

Who Should Consider a Conventional Loan?

If you have a strong credit history and can afford a larger down payment, a conventional loan might be your best option.

Government-backed loans, such as FHA, VA, and USDA loans, are designed to make homeownership more accessible.

FHA Loans: A great option for first-time buyers or those with lower credit scores. These loans require as little as 3.5% down.

Pros:

Cons:

VA Loans: Available to veterans and active-duty service members, VA loans offer 0% down payments and no PMI.

Pros:

Cons:

USDA Loans: Designed for rural homebuyers with low-to-moderate incomes, USDA loans offer 0% down payment for eligible areas.

Pros:

Cons:

Who Should Consider a Government-Backed Loan?

If you’re a first-time buyer, have a lower credit score, or qualify for VA or USDA loans, these programs may offer the most accessible path to homeownership.

Here are some tips to help you choose the right mortgage based on your personal circumstances:

Choosing the right mortgage is crucial to your home-buying journey. While each mortgage type has its pros and cons, the best option will depend on your financial situation and future plans. Take your time, compare options, and don’t hesitate to seek advice.

If this post clarified your mortgage options, share it with others in your network who might benefit. And if you need personalized advice, I’m always here to help guide you through your home-buying journey with confidence and clarity.

Thanks for joining me on Monday Mortgage Matters! Stay tuned for next week’s post as we continue breaking down the home-buying process step-by-step. Until then, stay informed and empowered!

Start Your New Home Search Now!

Stay up to date on the latest real estate trends.

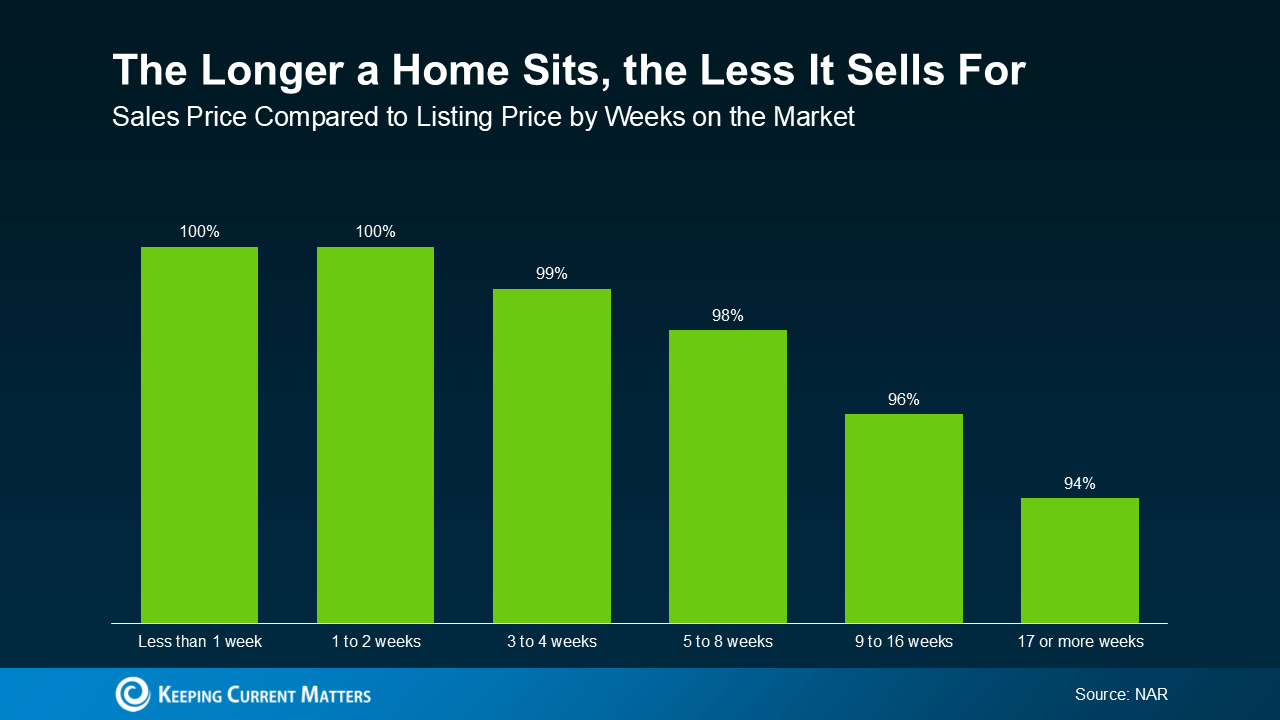

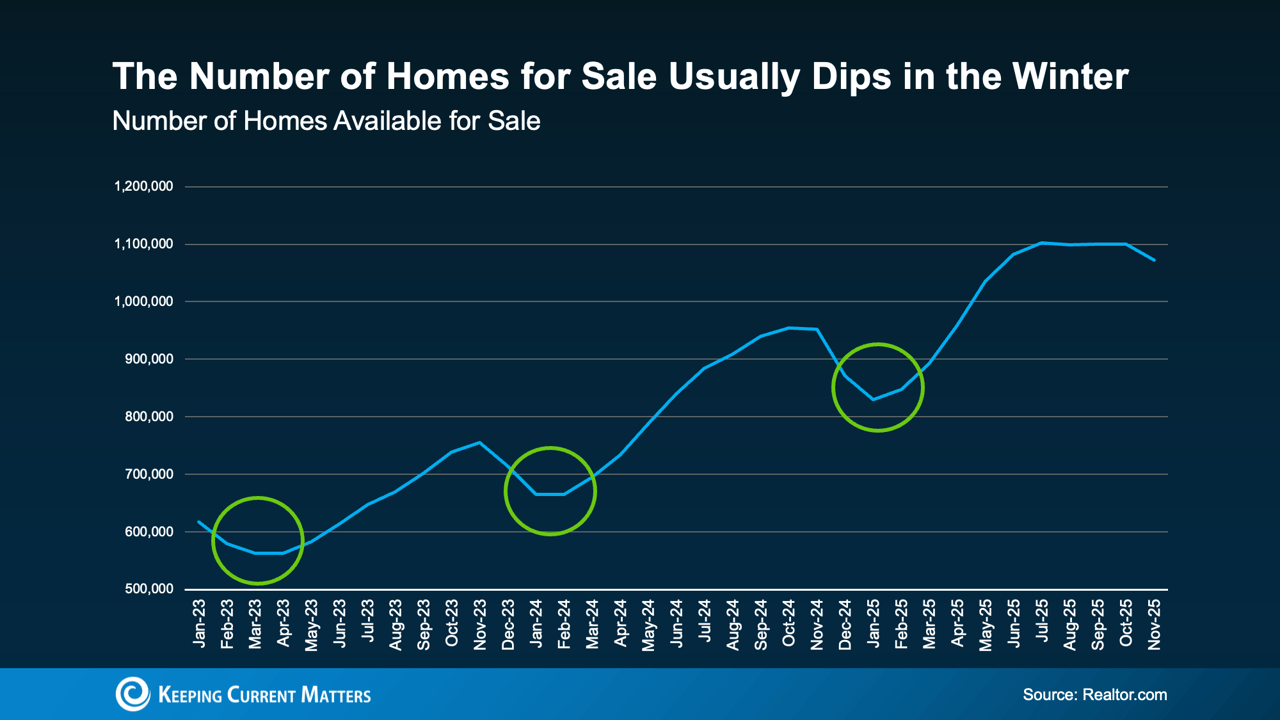

Why longer-listed homes can give Atlanta buyers more leverage and savings

Less Competition, Motivated Buyers, and a Head Start Before Spring

Homebuyer Tips

Boosting Your Home Value in Georgia

Home Selling Tips

Smart tips for Georgia homeowners selling in today’s market

You’ve got questions, and we can’t wait to answer them.