How Your Credit Score Impacts Mortgage Approval and Tips to Boost It

Personal Finance

Personal Finance

Welcome to another edition of Monday Mortgage Matters! Today, we’re tackling one of the most critical factors in the mortgage approval process: your credit score. Whether you’re buying your first home or upgrading to a new one, understanding how your credit score affects your mortgage options can have a significant impact on your home-buying experience.

In this post, we’ll break down what lenders look for in a credit score, how your score influences your mortgage terms, and actionable steps you can take to improve your score before applying. Let’s dive in!

Your credit score provides lenders with a snapshot of your financial health and your ability to manage debt. Typically ranging from 300 to 850, a score of 620 or higher is generally needed to qualify for most mortgage loans. Here’s how lenders evaluate your score:

Credit Score Ranges:

Key Factors That Affect Your Score:

Your credit score doesn’t just determine whether you qualify for a mortgage—it also plays a big role in the interest rate you’ll receive and the loan options available to you.

Interest Rates:

Loan Options:

Down Payment Requirements:

Improving your credit score before applying for a mortgage can make a big difference. Here are some actionable strategies to help you boost your score:

Pay Bills on Time:

Reduce Credit Card Balances:

Avoid Opening New Credit Accounts:

Check Your Credit Report for Errors:

Keep Older Accounts Open:

Consider a Secured Credit Card:

Your credit score is a key factor in your mortgage approval and the loan terms you’ll receive. By understanding its impact and taking proactive steps to improve it, you’ll be better positioned to secure a favorable mortgage that aligns with your financial goals.

Whether you’re just starting to think about homeownership or are ready to apply for a mortgage, use these tips to build a stronger financial foundation. If you found this post helpful, be sure to share it, and follow along for more insights in our Monday Mortgage Matters series.

As always, if you have any questions or need personalized advice, don’t hesitate to reach out. I’m here to guide you through your journey toward homeownership with confidence and clarity.

Thank you for tuning in today! See you next week as we continue to explore the ins and outs of the mortgage process. Stay informed and financially empowered!

Start Your New Home Search Now!

Stay up to date on the latest real estate trends.

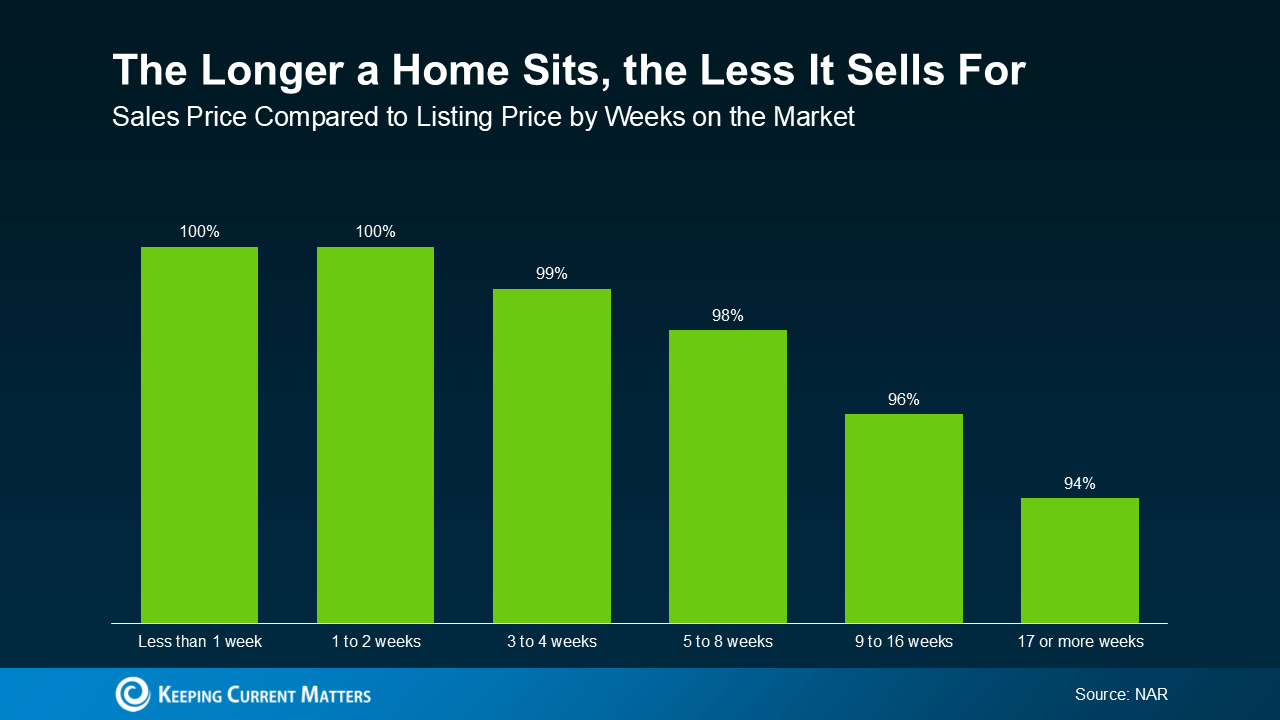

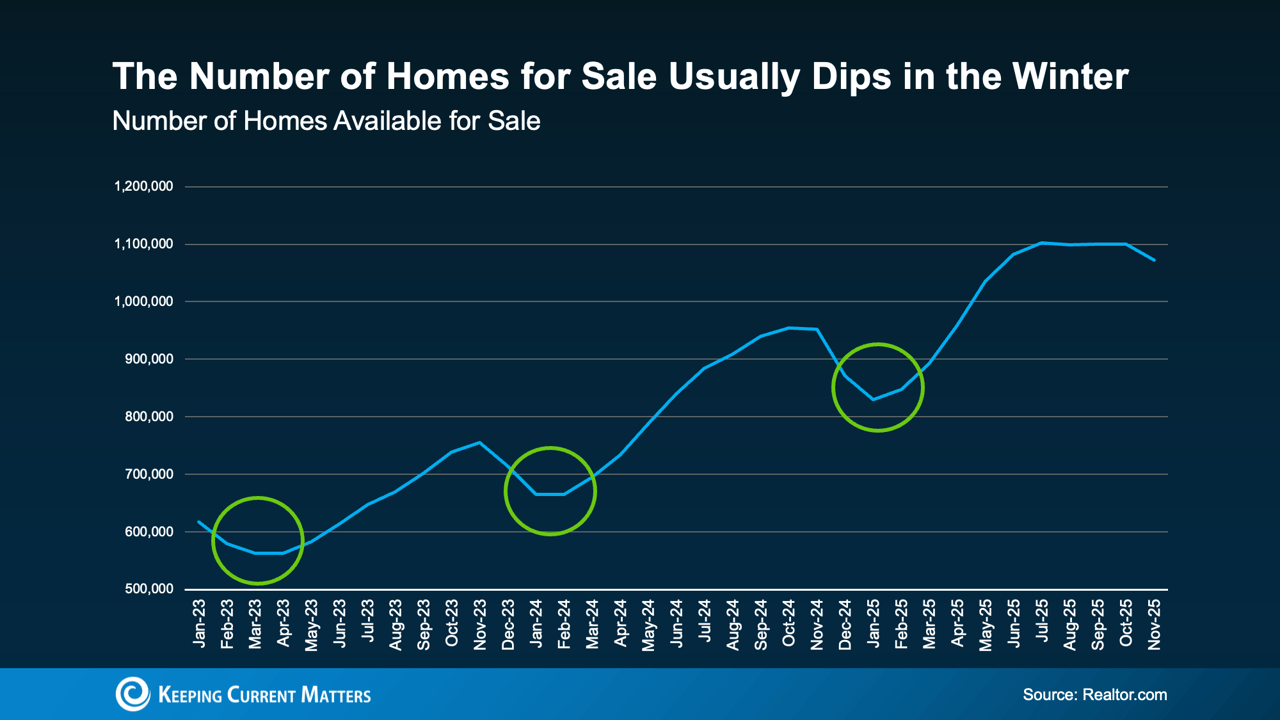

Why longer-listed homes can give Atlanta buyers more leverage and savings

Less Competition, Motivated Buyers, and a Head Start Before Spring

Homebuyer Tips

Boosting Your Home Value in Georgia

Home Selling Tips

Smart tips for Georgia homeowners selling in today’s market

You’ve got questions, and we can’t wait to answer them.